ZKsync (ZK)

ZKsync (ZK)

- 58مؤشر المعنويات الاجتماعية (SSI)- (24h)

- #80ترتيب اتجاه السوق (MPR)0

- 4الانتشار الاجتماعي 24 سا- (24h)

- 50%نسبة KOL الصاعدة خلال 24 ساعة4 مؤثر KOL نشط

- ملخصIn the past 24h, ZK price rose modestly by 2.9%, high-leverage bullish tweet activity is high, though there is overall L2 fatigue and regulatory privacy concerns.

- إشارات صعود

- 100x leverage bullish

- High interaction sentiment positive

- Price up 2.9%

- ZK relatively sturdy

- Privacy demand can be favorable

- إشارات هبوط

- L2 overall fatigue

- Market more pickier seeking evidence

- Regulatory privacy pressure

- Negative sentiment persists

- Institutional uncertainty

مؤشر المعنويات الاجتماعية (SSI)

- البيانات الإجمالية58SSI

- اتجاه SSI (7ي)السعر (7 أيام)توزيع المشاعرصاعد (50%)محايد (25%)هابط بشدة (25%)رؤى SSIZK social heat is moderate (58/100) and activity is high (35/40), positive sentiment modest (15/30), driven by high-leverage bullish tweets and a 2.9% price increase.

ترتيب اتجاه السوق (MPR)

- منبه الرؤىZK warning rank #80, social anomaly high (82.93/100) notable, KOL attention shift weak (7/100), linked to L2 fatigue and regulatory privacy concerns.

منشورات X

DEFI Fundamentals FA_Analyst DeFi_Expert B15.42K @Defifundamental

DEFI Fundamentals FA_Analyst DeFi_Expert B15.42K @DefifundamentalCustody Is the Quiet Gate Every Institutional Settlement Network Has to Clear First Most analysis of onchain settlement counts banks. The more useful thing to count is custodians, because a regulated institution cannot settle an asset it cannot first hold under its own compliance rules. This is the step that gets skipped in the excitement about tokenized deposits and tokenized funds. Settlement and custody are not the same problem. A bank can be convinced the rails are fast and final and still be unable to touch them, because its mandate requires qualified custody with specific controls over keys, segregation, and audit. No custody path means no participation, regardless of how good the settlement layer is. That is why the BitGo institutional custody and wallet integration with Prividium matters more than its size suggests. It is not one more logo. It removes the precondition that blocks every incoming institution before settlement is even on the table. Consider the order of operations a regulated entity actually follows: • It must custody the asset within a framework its regulator already accepts. • Only then can it settle, because settlement moves assets that have to be held somewhere compliant at rest. • Only then do network effects apply, because a corridor needs two institutions that can both hold and move. Seen this way, the deployments on @zksync rails are not parallel announcements. They are a sequence. Custody integration is the part that converts a settlement layer from a demo into something an incoming bank can actually onboard to, because the holding problem was solved before the bank arrived. The architecture underneath is what makes this hold together rather than a set of separate vendor relationships. Banks execute inside private environments where only zero-knowledge proofs and state commitments reach Ethereum, settlement is final without optimistic challenge windows, and the same stack carries custody, execution, and interop instead of stitching them across teams. Here is the part worth contesting: the institutional race in 2026 will not be decided by whoever has the fastest proofs or the most famous bank logo. It will be decided by whoever made it boring and compliant to hold the asset in the first place, because that is the step that quietly gates all the others. For anyone who has actually sat through an institutional custody and settlement review, which gate really decides whether a bank can join a network: the speed of settlement, or the holdability of the asset at rest?

47 21 380 أصلي >اتجاه ZK بعد الإصدارمتصاعد بقوةZKsync paves the way for large-scale institutional adoption of crypto assets by solving the institutional custody challenge.

47 21 380 أصلي >اتجاه ZK بعد الإصدارمتصاعد بقوةZKsync paves the way for large-scale institutional adoption of crypto assets by solving the institutional custody challenge. Tbros6868 Influencer Community_Lead B11.86K @tbros6868

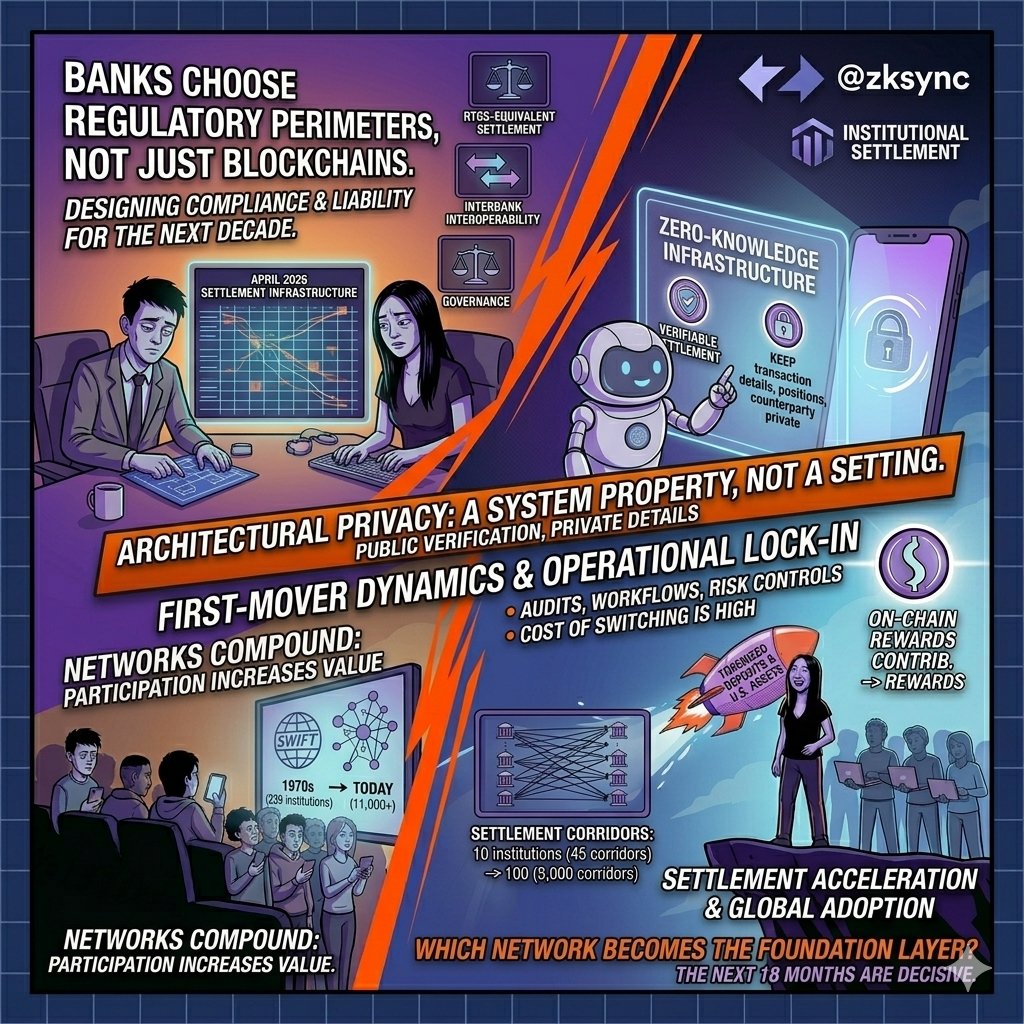

Tbros6868 Influencer Community_Lead B11.86K @tbros6868Banks aren’t choosing a blockchain. They’re choosing the regulatory perimeter they’ll operate inside for the next decade. That’s what the 2026 settlement infrastructure decision is really about. Right now, institutions are evaluating a set of unresolved questions that the April 2026 GFMA report identified as critical for institutional onchain finance: interbank interoperability for tokenized deposits, transaction privacy, RTGS-equivalent settlement, and governance for digital money. These are not isolated technical features. Together, they determine whether a settlement rail can support regulated financial activity across jurisdictions. Every rail exposes information differently. What a regulator can access, what a counterparty can infer, what an infrastructure operator can reconstruct. Those design choices shape compliance obligations, liability frameworks, and ultimately which markets a bank can operate in. This is why privacy has become a structural issue rather than a product feature. A privacy model that works for one jurisdiction may fail in another if confidentiality depends on permissions that can be altered later. For global institutions, privacy increasingly needs to be architectural: a property of the system itself rather than a setting that can be switched on or off. That changes the importance of zero-knowledge infrastructure. Instead of forcing institutions to choose between transparency and confidentiality, zero-knowledge systems allow settlement validity to be publicly verified while keeping transaction details, positions, strategies, and counterparty relationships private. Regulators can receive verifiable access without exposing sensitive information across the entire network. For banks evaluating long-term settlement rails, that distinction matters. The market opportunity is no longer theoretical. JPMorgan’s Kinexys platform has processed more than $1.5 trillion in transaction volume. DTCC is advancing tokenized Treasury infrastructure under existing regulatory frameworks. NYSE, BNY, and Citi are building tokenized securities rails. Meanwhile, the majority of tokenized U.S. assets already settle on Ethereum-based infrastructure. The institutions entering these networks today are not simply choosing technology. They are helping define the standards future participants will inherit. That is where first-mover dynamics become powerful. Financial infrastructure compounds differently from consumer technology because adoption creates operational lock-in. Once a bank integrates a settlement rail, the costs of switching extend far beyond software migration. Institutions must repeat audits, satisfy regulators, rebuild operational workflows, renegotiate counterparty agreements, and re-establish risk controls that may have taken years to construct. History shows how durable these effects can become. SWIFT began with 239 institutions in the 1970s. Today it connects more than 11,000 financial institutions globally. Its dominance was not driven by superior technology alone. It persisted because every new participant increased the value of the existing network while raising the cost of choosing an alternative. Settlement infrastructure follows the same logic. Ten institutions create 45 potential settlement corridors. One hundred create nearly 5,000. Each additional participant increases not only transaction volume but also the number of relationships available through the network. The result is an asymmetry where the leading network's advantage compounds faster than competitors can replicate. This is why @zksync is worth watching in the institutional race. Its zero-knowledge architecture addresses one of the most difficult constraints identified by global financial institutions: achieving verifiable settlement while preserving confidentiality across jurisdictions. As more regulated deployments move onchain, infrastructure capable of satisfying both regulatory oversight and privacy requirements becomes increasingly valuable. The key question is no longer whether institutional finance moves onchain. That transition is already underway. The question is whether privacy-preserving settlement standards can achieve sufficient adoption before regulatory fragmentation hardens into separate regional systems. History suggests that once regulated institutions converge on a settlement standard, displacement becomes increasingly uneconomic. The next 18 months may determine which networks become the foundation layer for institutional settlement in the decade ahead.

43 31 2.42K أصلي >اتجاه ZK بعد الإصدارصاعدzkSync has a leading advantage in institutional settlement due to its zero-knowledge architecture, and the next 18 months are critical.

43 31 2.42K أصلي >اتجاه ZK بعد الإصدارصاعدzkSync has a leading advantage in institutional settlement due to its zero-knowledge architecture, and the next 18 months are critical. Tanaka FA_Analyst Influencer B45.63K @Tanaka_L2Tanaka FA_Analyst Influencer B45.63K @Tanaka_L2

Tanaka FA_Analyst Influencer B45.63K @Tanaka_L2Tanaka FA_Analyst Influencer B45.63K @Tanaka_L2The market is becoming more selective. I think the easy narrative trade is getting weaker because investors now want proof. A clean story can still attract attention, But attention alone does not create durable repricing. The comparison is simple: On one side, you have tokens where the narrative came first and the usage never caught up. The market has been brutal to that bucket: → $ZK, $STRK, $BLAST, $KAITO, $PLUME, $BERA, $LINEA each is down **~96-99% from ATH.** → All had narratives people understood, but the market no longer pays full price for projected adoption. I don’t think the market rejected these sectors from first bucket completely. AI attention, RWA, liquidity design, and ZK infra are still valid narratives. The problem is that narrative without revenue, user retention, real demand, or capital flow becomes hard to defend when liquidity tightens. When the market is risk-on, people buy future potential. When the market becomes selective, people find real tractions such as revenue, usage,

89 28 9.25K أصلي >اتجاه ZK بعد الإصدارصاعدThe market is shifting from pure narrative to emphasizing actual project value and data support, and tokens with real use cases perform better.

89 28 9.25K أصلي >اتجاه ZK بعد الإصدارصاعدThe market is shifting from pure narrative to emphasizing actual project value and data support, and tokens with real use cases perform better. VietnamPenguin Derivatives_Expert OnChain_Analyst S3.82K @VietnamPenguin

VietnamPenguin Derivatives_Expert OnChain_Analyst S3.82K @VietnamPenguinI've spent a lot of time thinking about $ZK. There's a ton of negativity around the token, but if we're being objective, the problem isn't ZK token itself. The problem is that the entire L2 sector looks cooked right now.. with MEGA feeling like the final nail in the coffin. In fact, compared to many other L2s, $ZK has held up surprisingly well. The real question is: does the L2 meta ever come back? 👀

1 2 586 أصلي >اتجاه ZK بعد الإصدارمحايدThe L2 sector overall performed poorly, but ZK showed relative resilience, and the author holds a long position.

1 2 586 أصلي >اتجاه ZK بعد الإصدارمحايدThe L2 sector overall performed poorly, but ZK showed relative resilience, and the author holds a long position. MadMaxx (∎, ∆) OnChain_Analyst Tokenomics_Expert B13.66K @MadMaxx_eth

MadMaxx (∎, ∆) OnChain_Analyst Tokenomics_Expert B13.66K @MadMaxx_ethPutting it all into ZK on 100x leverage https://t.co/uheicR309A

wale.moca 🐳 OnChain_Analyst Tokenomics_Expert B175.21K @waleswoosh

wale.moca 🐳 OnChain_Analyst Tokenomics_Expert B175.21K @waleswooshCT is so dead that all I see on the timeline this morning are two-figure X creator payouts

88 45 3.20K أصلي >اتجاه ZK بعد الإصدارهابط بشدةThe author feels hopeless about the market slump, betting on ZK with 100x leverage and showing minimal income. ZKsync Founder Regulatory_Expert D1.47M @zksync

ZKsync Founder Regulatory_Expert D1.47M @zksyncJUST IN: $ZK, the native token of ZKsync, is now live on @Bitstamp. https://t.co/JyYUHgc6Ov

Bitstamp by Robinhood D515.87K @Bitstamp

Bitstamp by Robinhood D515.87K @BitstampNew asset now available to trade on Bitstamp by Robinhood. $ZK (ZKsync) https://t.co/AmT4A64EeY

260 24 88.94K أصلي >اتجاه ZK بعد الإصدارصاعدThe native ZK token of ZKsync is now listed on the Bitstamp exchange, increasing its trading accessibility.

260 24 88.94K أصلي >اتجاه ZK بعد الإصدارصاعدThe native ZK token of ZKsync is now listed on the Bitstamp exchange, increasing its trading accessibility. Leafswan NFT_Expert Community_Lead C63.49K @leaf_swan

Leafswan NFT_Expert Community_Lead C63.49K @leaf_swanGM and welcome to some morning Web3 knowledge pill! Everyone keeps asking which blockchain institutions will choose, but I think that's the wrong question because the real decision is which settlement rail can satisfy regulators, banks, custodians, and asset managers all at once? Right now @zksync is the only network with production institutional deployments spanning Deutsche Bank's Memento platform, ADI Chain, and BitGo. What's next? Cari Network is currently onboarding five U.S. regional banks representing $600B+ in deposits with production rollout planned for later in 2026. When privacy, cryptographic finality, institutional control, and interoperability are built into the same stack, the success of the infrastructure is guaranteed! Here's my take, so let me know what you think!

24 23 309 أصلي >اتجاه ZK بعد الإصدارمتصاعد بقوةzkSync is the only institution-grade deployed network, expected to become a mainstream settlement layer in the future.

24 23 309 أصلي >اتجاه ZK بعد الإصدارمتصاعد بقوةzkSync is the only institution-grade deployed network, expected to become a mainstream settlement layer in the future. CryptoMage 🧙♂️ Trader Educator B15.22K @CryptoMage_YT

CryptoMage 🧙♂️ Trader Educator B15.22K @CryptoMage_YTSatori, which we used back in the ZkSync era, is going to shut its doors; check if you still have any funds there even though I doubt it.

Satori D180.42K @SatoriFinance

Satori D180.42K @SatoriFinanceA Heartfelt Farewell from Satori Finance Dear Satori Finance Users, After careful consideration, we have made the difficult decision to wind down Satori Finance operations. Our team has poured tremendous effort, passion, and countless hours into building and growing this platform. Unfortunately, due to prolonged unfavorable market conditions, our revenue has not been sufficient to sustain operations, and continuing to run the platform is no longer financially viable. We want to reassure you that your assets remain fully safe and under your control throughout this transition period. There is no need for concern — this notice is simply to help you plan ahead and ensure a smooth, orderly withdrawal process. A withdrawal and position-closing window will be open from June 16, 2026, 23:59 UTC to July 16, 2026, 23:59 UTC. We kindly encourage all users to close open positions and withdraw their assets at their earliest convenience during this period, to make the process as smooth as possible for everyone.

15 3 4.29K أصلي >اتجاه ZK بعد الإصدارهابطZKSync platform Satori is about to close, please withdraw assets promptly. 蓝狐 FA_Analyst Influencer B73.40K @lanhubiji

蓝狐 FA_Analyst Influencer B73.40K @lanhubijiSeeing the ZKSync layoffs is bittersweet. ZKSync was one of the strongest Ethereum L2 projects at the time, with leading EVM compatibility, native account abstraction support, and efficient ZK proofs. If historically it hadn't been delayed, had issued tokens before Arbitrum and leveraged economic mechanisms to support ecosystem projects, would the outcome have been different? Of course, ZKSync is now contracting its front lines and undergoing a transformation: its TVL still has some scale (Era + Elastic Network together exceed 1 billion in economic value), RWA development is ongoing, the ZK Stack is being adopted across multiple chains, and ZKnomics is attempting to build a sustainable economic cycle. However, compared to Arbitrum/Base, its share is indeed smaller. Focusing on institutions is also an unavoidable choice; pursuing a path of compliance + privacy + tokenization may be the breakthrough.

ALEX | ZK D52.17K @gluk64

ALEX | ZK D52.17K @gluk64Today we reduced the size of the Matter Labs team. This was my decision, and I want to explain it. In 2024 we began building for regulated financial institutions. That work became Prividium, and the entire company is now committed to one goal: building the infrastructure that brings enterprises and regulated financial institutions onchain, with privacy at its core. As that work has progressed, we have learned a great deal about where our customers need it to go. Meeting that direction calls for a different mix of skills and roles than the phase before it, and some of what made sense earlier is not what we need now. That is the reason for today's changes. It hurts, because this is not about the effort or talent of the people leaving, who I deeply respect. They are some of the strongest engineers, designers, and operators I have worked with. Everyone leaving has been offered financial support, and we are helping with the transition wherever we can. If you are hiring, you can request access to our opt-in ta

47 41 26.47K أصلي >اتجاه ZK بعد الإصدارهابطZKSync layoffs shrink operations, short-term outlook under pressure, focusing on compliance finance 토큰포스트 - TokenPost Korea Media Influencer D5.73K @tokenpostkr

토큰포스트 - TokenPost Korea Media Influencer D5.73K @tokenpostkrMatter Labs, undertaking restructuring… focusing on institutional on-chain privacy infrastructure https://t.co/CWWDsWFvAd https://t.co/s9FtQmJktM

0 1 23 أصلي >اتجاه ZK بعد الإصدارمحايدMatter Labs restructuring, focusing on institutional-grade on-chain privacy infrastructure.

0 1 23 أصلي >اتجاه ZK بعد الإصدارمحايدMatter Labs restructuring, focusing on institutional-grade on-chain privacy infrastructure.